A plethora of financial instruments exist that allow people or entities to interchange cash flows. The instruments come with varying bank payments as well as the duration to maturity. Currency swaps and interest swaps are such contracts that offer an ideal way of borrowing capital for various purposes at desired terms.

Interest swaps are derivative contracts in which two entities enter and agree on how they will exchange bank costs on cash flows. In this case, lending overheads are bartered between two parties involved in the agreement. They can be fixed or floating.

Such contracts come with clearly spelled out terms of the agreement detailing the price of money each party on the deal is entitled to or required to pay. The contracts must also describe the start date and maturity date of the agreement.

It is commonly leveraged by corporations, banks, and investors looking to profit from perceived ideal charges in the market. Additionally, they are widely used to hedge against variable annual percentage costs.

For instance, if someone has a loan financed through a variable charge, they are constantly in the dark over the amount of borrowing cost they are likely to pay in the future, given the fluctuating tariffs. Changes in the price of money can significantly affect the borrowing costs, making it difficult to prepare the loan in advance. Interest swaps are widely used to curb the negative impact of fluctuating charges.

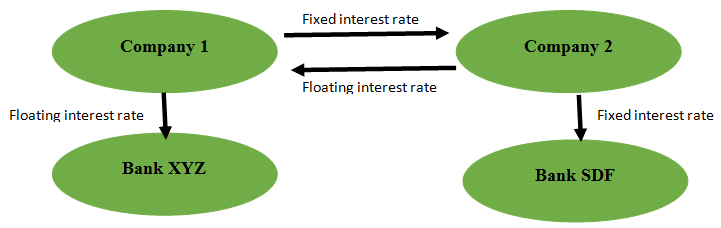

Additionally, the interest rate trade can come into play when one party receiving fixed overheads and another party receiving floating outflows decides to interchange their lending charge payments. This would occur when the party receiving floating-rate feels they would be better off if they are guaranteed fixed disbursements over a given period.

Similarly, the person receiving fixed-charge outlays would opt for floating charge payments if they feel fluctuating outflows have a higher prospect of increasing in the future.

How do they work?

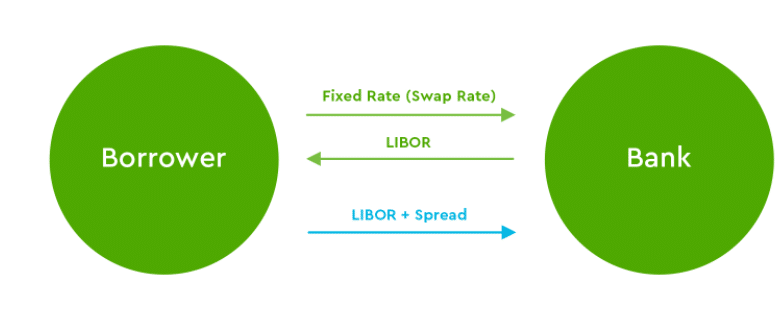

Interest swaps are commonly used to turn the borrowing cost one is required to pay on a variable rate loan into a fixed fee or vice versa. In this case, a trade-off occurs between lending charge payments between the loan borrower and lender. However, the two parties don’t trade the principal amount but the lending costs.

A borrower must pay the variable borrowing charge on the amount borrowed every month with an interest swap. Additionally, the borrower must make disbursements to the lender based on an agreed swap charge. The exchange rate does not change from month to month, and the borrower is required to make payments on the required amount.

At the end of the loan, the lender is required to rebate the variable-rate amount. In this case, the borrower ends up incurring a fixed charge on loan outlays.

Benefits

Interest swaps are great to use when an entity wants to negate the impact of higher borrowing costs. Once a swap rate is set, one can know the amount of money required to pay each month.

A traditional fixed-rate loan only guarantees the rate for a specific period. In contrast, a rate on an interest swap can be locked and set to start on a date in the future. In this case, one can secure a rate that could begin months or years later.

Finally, it can be secured and set to begin on a portion of a loan. Unlike normal lending plans, it does not have to last the entirety of a loan.

Currency swap

A currency swap is also a derivative contract that entails the exchange of loan charge payments. However, unlike interest trades, it also involves the exchange of principal amounts at a later date. In most cases, the principal amounts are denominated in different currencies.

They consist of fixed and floating payments in two different currencies. The transfer of the agreement reached between the two parties involves the outlays at a predetermined date in the future.

Example

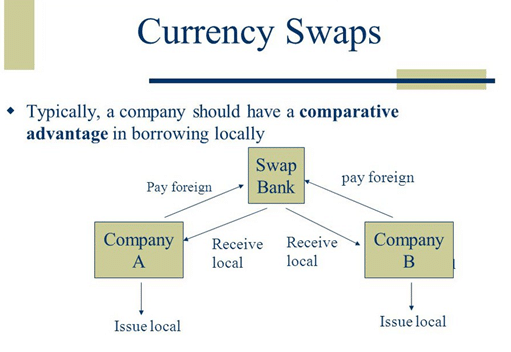

Consider company A planning to carry out an acquisition worth £700,000 in Europe. On the other hand, corporate B plans to purchase a business worth $1 million in the US. If the two entities don’t have sufficient money, they will have to venture into the debt market to raise the required amount.

A currency swap will have to come into play if the two wish to benefit from borrowing within their respective jurisdictions.

In this case, company A can pursue a $1 million credit line in the US from Bank X at a fixed rate of 2.5%. On the other hand, Corporate B can obtain a £700,000 credit line in Europe at a floating charge of 6-month LIBOR.

Company A and corporate B can come together and carry out a currency interchange with the two credit lines in place. After that, they will trade off the outlays with company A, paying a floating charge of 6-month Libor and corporate B making payments for the fixed 2.5% charge.

Company A will end up paying corporate B floating payments in euros. In return, B will pay company A the fixed payments in US dollars. At maturity of the loan, the companies will exchange back the principal amount at the same cost of $1=£0.7

Benefits

Currency swaps come in handy in the redenomination of loans or other payments from one coinage to another. In most cases, they allow corporations to raise funds in one exchange and make savings in another by simply exchanging.

Additionally, they are used to hedge the risk associated with other currencies, while also being able to lock in fixed exchange charges for a longer period. The risk of carrying out changeovers is usually small, and the contracts are usually highly liquid as they can be settled at any time.

Bottom line

Interest and currency swaps are derivative contracts that entities enter in a bid to trade-off cash flows and bank charge payments. The trades that come into play allow firms to secure low-cost loans and hedge against perceived lending costs fluctuations.

{kind=link}